How omnichannel banking drives customer engagement in retail banking

Participants in a recent survey said banks aren’t engaging retail customers. Here’s how omnichannel banking can help engage retail banking clientele.

Retail banks are facing a challenge. In Accenture’s Global Banking Consumer Study nearly 63% of the surveyed 49,000 banking customers worldwide said they only log into mobile apps to check their account balances. This is indicative of a severe lack of omnichannel banking capabilities.

It gets worse. Only 25% said their bank performs ‘extremely well’ when it comes to keeping up with important changes to their personal finances. Meaning that around 75% of customers don’t feel sufficiently engaged.

Customer needs are changing, and two-thirds of respondents said their banks are not responding to these evolving needs quickly enough.

Fintech companies are picking up the slack, and are catering to underserved retail banking customers. These companies are providing quick access to financial services while also paying attention to new needs, keeping their users engaged.

But all is not lost. There is a way to improve customer engagement in retail banking. There are customer engagement strategies in banking that are already being used to keep clients informed, secure, and engaged. And it can be as simple as texting your client.

What is omnichannel banking?

Omnichannel banking refers to creating a holistic customer experience by integrating all touchpoints, including digital and personal interactions. This results in consistent, personalized, and informed user experiences, regardless of channel.

Omnichannel vs multichannel banking

This is different from multichannel banking. In multichannel banking, services may be made available across a variety of touchpoints, but these aren’t integrated.

For example, in multichannel banking, a client can apply for a loan using their banking app; but if they want to continue this process in a branch, they may need to restart their application.

With omnichannel banking, however, the process simply flows from app to branch without frustrating interruptions.

This common example demonstrates how critical omnichannel customer engagement strategies in banking can be.

Key characteristics of a successful omnichannel banking strategy

Developing a successful omnichannel banking strategy relies on the seamless interactivity of all its touchpoints.

All your available channels need to feed into a central nervous system – typically a customer data platform – where all interactions are stored and made available to other channels.

Using our previous example, when a customer applies for a loan using their app, everything is waiting for them at the branch when they go meet with their personal banker.

This seamless interaction between channels extends to other parts of your clients’ customer journey, as well. Support is a common example.

A client may engage with a chatbot to request support regarding a suspicious transaction. Since this is a very serious issue, your chatbot may likely be programmed to involve a specialized agent from your bank’s claims department.

In a multichannel environment, the client will have to start the whole story over and repeat the details of their claim to the agent. This can be very frustrating given the circumstances.

However, in an omnichannel banking scenario, the transfer between an automated chatbot assistant to a human agent – is seamless. The conversation continues in the same chat app with the context and details preserved for fast resolution.

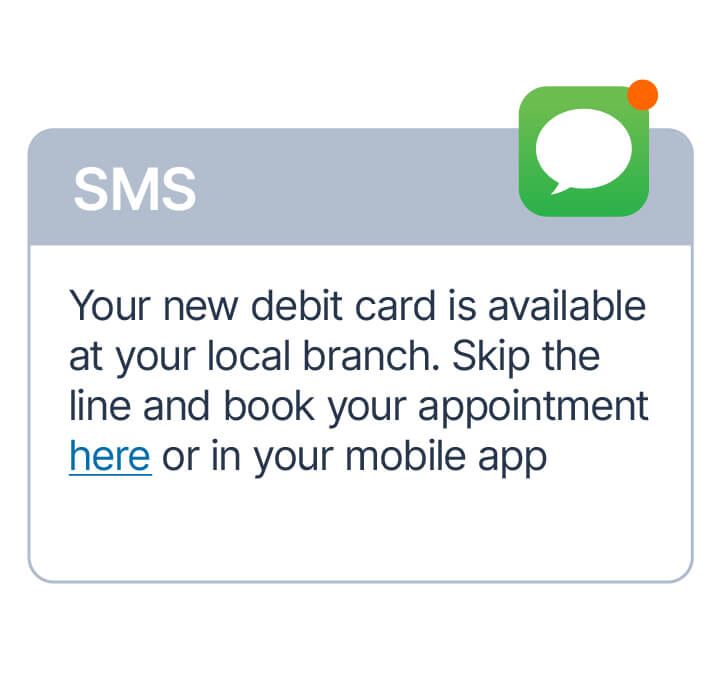

Next in this specific scenario, the client may be issued a new card. This info is visible in the client’s history, so when they go to the branch to pick up their new card in person the process is made fast and easy.

What do you need for omnichannel banking

The cornerstone of an omnichannel banking strategy is having customer data in a centralized database that is constantly updated from all touchpoints.

For example, some organizations have customer data siloed across different customer-facing departments. This can lead to certain challenges if data is not collated into a centralized database.

Addressing this will allow banks to use information from all their departments to build and nurture up-to-date customer profiles that facilitate omnichannel banking activities.

With customer data properly collected, stored, and made accessible across the organization, banks then need to partner with channel providers to engage customers digitally.

This step involves identifying CPaaS providers with experience in providing communication platform services to the financial sector and who can satisfy strict criteria in terms of security, local and global legislation, data privacy protection, etc. Additionally, look for providers with a proven track record of offering fast, expert support – ideally locally and in your local language – to assist with integration into your existing technology stacks.

It may seem like a lot of work – and it’s no small task – but this is why it’s best to partner with a proven provider. Because the benefits, which we’re about to get into – are massive.

Benefits of omnichannel banking for customer engagement

To improve customer engagement in retail banking, clients expect banks to meet them where they are. Facilitating this customer engagement activity in banking will reap the following benefits:

- Convenience and choice: Clients can engage their bank using the channels and methods they prefer for secure transactions and interactions. For example, a client can book a meeting with their personal banker using their app. This appointment will then be scheduled in their personal banker’s calendar with the client’s full customer history for a quick and efficient meeting. After this the client can receive an email recapping the meeting with any next steps clearly defined.

- Personalized experience: By collecting customer data across all touchpoints and making it available in a single place, banks can empower human and automated agents to provide personalized experiences. For example, by accessing a client’s financial information and transaction history, agents can provide financial advice that is best suited to the client’s finances. This financial pulse check results in a better experience for clients who can be serviced with banking instruments that are best suited to their needs.

- Improved customer journey: Having access to up-to-date customer data collected across all touchpoints facilitates friction-free interactions. For example, a bank can detect a potentially fraudulent transaction in real-time and notify the client, requesting to confirm or cancel it. In the latter case, the bank can also offer to cancel the card being used in the transaction, offer to issue a new one, and ask the client whether they would like it delivered to their home address, office, or nearest branch. This reduces an otherwise lengthy process to a few short steps that keep the bank and customer protected.

- Increased customer satisfaction and loyalty: Adopting an omnichannel banking strategy allows clients to engage with your bank on their terms for faster and more satisfying experiences. For example, clients can engage with a chatbot for basic information. This results in fast resolution times that all customers appreciate. This interaction is then stored and “remembered” by the bank in case further assistance is needed. This leads to more personalized experiences, which improve customer loyalty.

These are just some of the most common benefits retail banks enjoy when they implement an omnichannel strategy. Next, let’s look at some customer engagement activities and strategies banks can employ.

Customer engagement strategies powered by omnichannel banking

Omnichannel capabilities can take common customer engagement strategies and dial them up to 11. Here are some ways omnichannel strategies in banking can be used to boost customer engagement.

- Proactive communication: Banks can proactively engage customers to help keep their accounts secure whenever suspicious activity is noticed. But it’s not all red alerts – by using customer history and analyzing financial data, banks can notify clients that they’re eligible for new lines of credit, higher interest savings accounts, or other banking products that reflect a client’s current financial state.

- Real-time engagement: Clients can get customer support in real-time – especially helpful when filling out lengthy and complex loan applications. Some apps allow for screensharing that can help agents guide clients through the otherwise demanding processes and provide critical information throughout.

- Data-driven insights: Offer clients personalized offers with targeted promotions, product recommendations, and loyalty programs based on client history, product browsing, financial status, behavioral triggers and more to increase their adoption and improve customer stickiness.

- Gamification and interactive experiences: Help clients achieve their goals – and yours – by making gamification a part of their customer journey. Accelerate customer onboarding by gamifying product education, and use reminders to help keep clients on track to achieving goals – regardless of whether these are personal financial goals or understanding how to leverage new banking products.

Conclusion

Currently, most customers don’t feel as though they’re being fully engaged by their banks. From the 63% who told Accenture’s study that they only use their bank app to check their status, to the three-quarters who implied their bank can do more to keep them engaged – adopting an omnichannel retail banking strategy will serve to boost engagement, increase loyalty, grow product adoption – and many more benefits to retail banks and their clients.

Discover how else banks benefit from our omnichannel platform

Omnichannel customer service: Unlock a 5-star experience.

From hype to hero: How chatbots can revolutionize your bank's customer experience.

Demystifying finance AI chatbots for fintech firms.

The impact of chat banking on Zenith Bank's digitalization journey.

The rise of conversational banking: Customer engagement trends for 2024.

How messaging trends are transforming banking in Malaysia.