WhatsApp Payments: Supported countries, API, peer-to-peer and business news updates

Discover how Payments on WhatsApp is not only making transactions more convenient but also bringing conversational commerce to life on your customer’s favorite channel.

Imagine chatting with your favorite retailer about the latest trends and buying the perfect outfit without leaving the conversation. Or managing your insurance or bill payments right in the same chat.

Payments on WhatsApp makes this real and brings conversational commerce to life on your customer’s favorite channel. In other words, your customer’s next purchase is no longer a checkout page. It’s simply the next message in the conversation.

Behind the simple “Pay” button in WhatsApp, there are actually two different products at work. Payments on WhatsApp is a business-payments feature for companies using the WhatsApp Business Platform. WhatsApp Pay is a peer-to-peer payment feature for personal transfers. They live in the same app but serve different needs. In the next sections, we’ll cover each one, where they are available, and how to set them up.

What is Payments on WhatsApp?

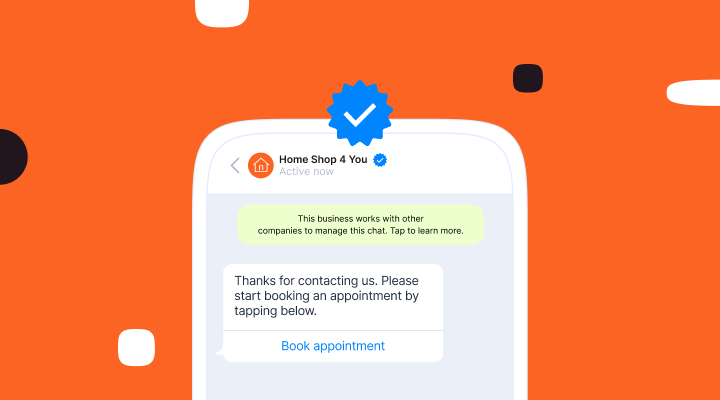

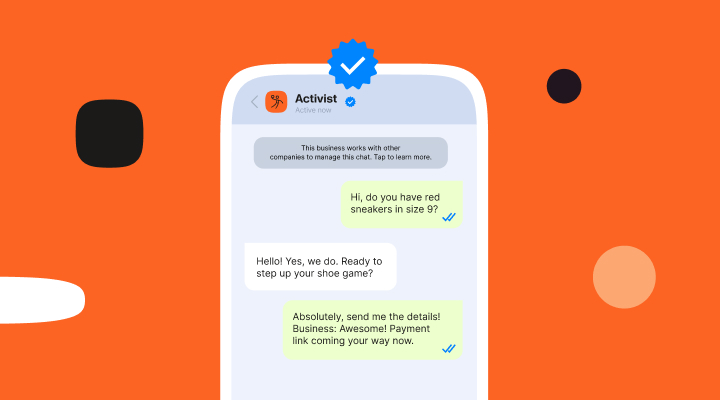

Payments on WhatsApp lets businesses accept customer payments directly inside a WhatsApp chat. It turns WhatsApp from a messaging app into a complete commerce channel, from product discovery to checkout and confirmation, all in one thread.

Next, it’s important to see how this plays out in different countries and payment ecosystems.

Supported payment methods by market

Before you decide on your flow, check what methods your customers prefer and what local rules require.

- India: UPI, debit and credit cards, net banking. Business payments typically connect through a payment gateway. P2P runs over UPI.

- Brazil: Debit and credit cards and supported bank methods through payment partners. P2P also runs locally with supported cards and bank accounts.

- Other markets: Availability is limited. Some partner-led pilots exist. Always verify support and providers before launch.

With the methods in mind, here’s how an end-to-end in-chat payment flow actually works.

How it works end-to-end

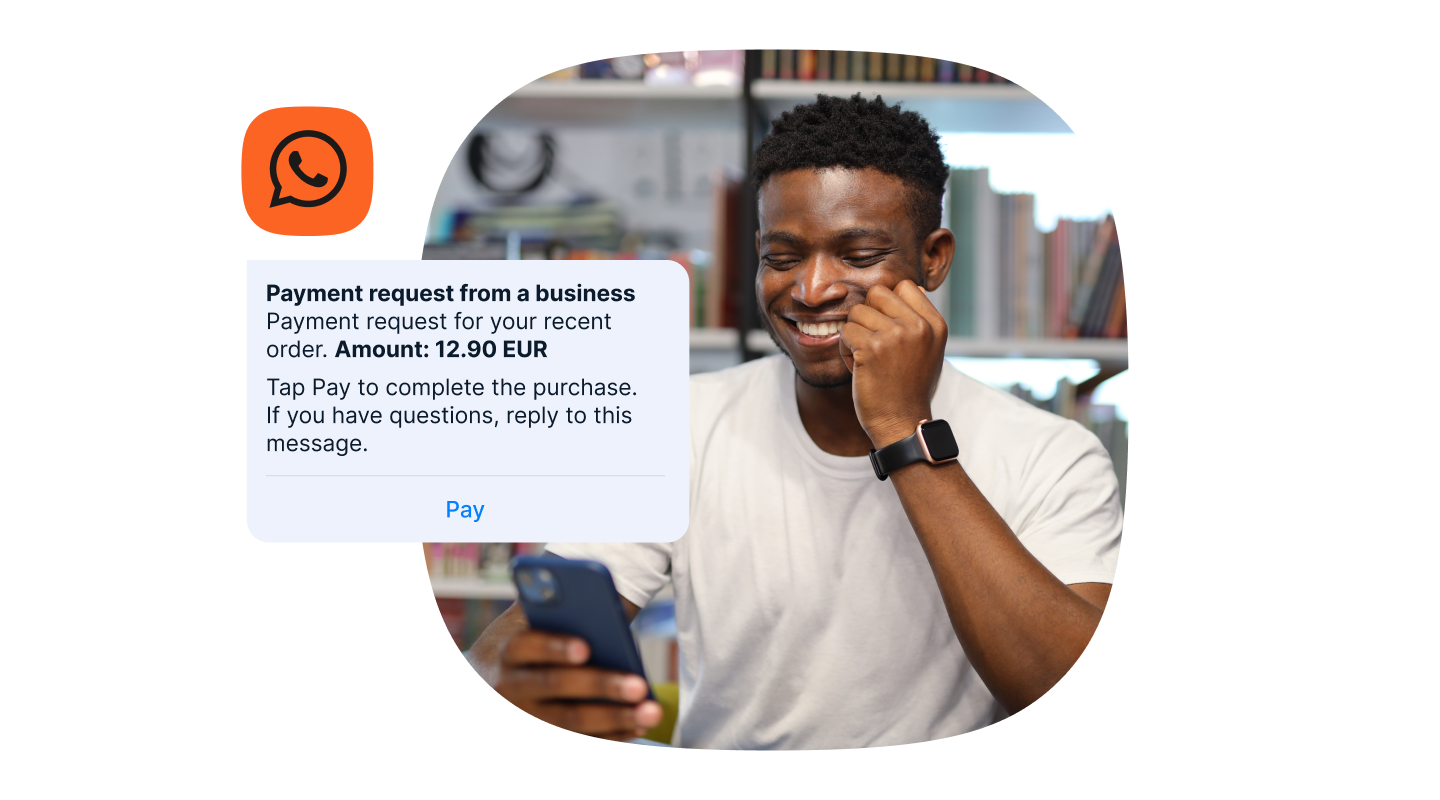

Set up a guided purchase flow with a catalog, cart, and checkout inside chat. Customers review items, choose a payment method, complete authentication, and receive instant confirmation without switching apps.

In Brazil, Payment Links let you generate a secure link in chat and track status. In India and Brazil, QR-code payments now allow customers to scan a code shared in chat and pay quickly.

Next, let’s clarify how WhatsApp Pay works for person-to-person payments.

What is WhatsApp Pay? (P2P payments)

WhatsApp Pay is for personal money transfers between individual users. It is designed for simple, secure peer-to-peer payments inside the WhatsApp app.

Here’s a quick look at the in-app setup for users in supported markets.

Step by step: sending and receiving money

Start with the in-app setup so you can send and receive money in chat.

- India: Go to Settings, then Payments, then Add bank account. Select your bank, verify via SMS, and set or confirm your UPI PIN. To send money, open a chat, tap the rupee icon, enter the amount, and confirm with your UPI PIN.

- Brazil: Go to Settings, then Payments, then add a debit or credit card. Create your Facebook Pay PIN. To send money, open a chat, tap the payment icon, enter the amount, and confirm with your PIN.

Where WhatsApp Pay works

P2P payments are currently available in India and Brazil. The experience, limits, and supported methods vary by country, bank, and partner.

To put this in context, here’s how support differs across key markets.

Availability by country

Availability depends on local regulation, banking partners, and WhatsApp’s rollout plans. Here is a quick view of where things stand today.

| Country/Region | P2P payments | Business payments | Notes |

|---|---|---|---|

| India | Available | Available | UPI for P2P and business payments. Cards and net banking supported for business via gateways. Per-transaction limit of ₹100,000 and daily volume limits apply. |

| Brazil | Available | Available | Cards and supported bank methods via partners. Per-transaction limit of R$1,000 and monthly caps apply. |

| Singapore | Not available | Limited partner-led pilots only | Verify current status with your payment provider before launch. |

| Future markets under consideration* | Not launched | Not launched | Mexico, UK, USA, Guatemala, Indonesia. Meta has explored expansion but no official launch dates. Some rollouts have stalled. |

*Future markets: Mexico, UK, USA, Guatemala, Indonesia.

These country differences are driven largely by regulation and limits. Here’s what to watch.

Regulatory requirements and transaction limits

Local regulators set rules for limits, verification, and fees.

In India, typical limits include ₹100,000 per transaction and up to 20 transactions per day for P2P. In Brazil, limits often include R$1,000 per transaction with monthly caps, which can vary by bank. For business payments, your payment gateway and acquiring bank set merchant fees and additional controls.

With the rules in mind, here’s what you need in place before enabling payments.

Business onboarding prerequisites

To enable business payments, you need:

- A verified Facebook Business account,

- Access to the WhatsApp Business Platform

- Approved payment partners, and compliance with local regulations.

With the basics covered, it’s time to look at what’s new and changing.

Recent news and updates (2024–2025)

WhatsApp payments continue to evolve fast. These updates matter for both SMBs and enterprises that want to close the loop from chat to checkout.

QR-code payments for small businesses in India and Brazil

In September 2025, Meta introduced QR-code payments for small businesses in India and Brazil. Merchants can generate and share QR codes in the WhatsApp Business app so customers can pay with cards, bank accounts, or wallets without leaving the chat.

Multi-device payments

In October 2025, WhatsApp enabled payments from linked devices like desktop and tablet without the primary phone being online. In India, support expanded for cards and third-party UPI apps, making checkout more flexible.

Removal of the user cap in India and adoption data

The user cap for WhatsApp Pay in India was removed, but adoption remains measured. Around 67 million UPI transactions were recorded in June 2025, signaling room for growth as features and partnerships mature.

Stablecoin and cross-border micro-payments exploration

Meta is exploring stablecoin use cases and cross-border payouts. Expect more focus on international disbursements and micro-transactions, but no production timelines have been announced.

These changes make the value even clearer. Here are the key benefits for your business.

Benefits of payments on WhatsApp

In-chat payments remove friction and boost completion rates. Customers stay in one conversation from discovery to payment.

- Streamlined end-to-end shopping journey within chat, including instant confirmation

- Higher conversion rates and fewer drop-offs at checkout

- Enhanced security with UPI PIN, two-factor authentication, and end-to-end encryption

- Better customer engagement with personalized flows and real-time support

- Global reach on a familiar messaging channel customers trust

Here’s how different industries are already putting these capabilities to work.

Use cases across industries

You can bring the entire journey into chat, from intent to payment, across different sectors.

Retail and e-commerce

A customer can ask about a product, see details and photos, get a personalized recommendation, and checkout on the spot with Payments on WhatsApp. This reduces cart abandonment and confirms the order in chat.

Financial services

Banks and insurers can enable balance inquiries, transaction history, bill payments, loans, and policy renewals. Customers complete secure payments within the same thread.

Public transportation

Transit providers can sell tickets in chat and confirm boarding instantly. For example, Vai de Bus in Brazil lets riders purchase and receive passes via WhatsApp, cutting queues and improving the rider experience.

Restaurants and local businesses

Customers can order, receive a payment link or QR code, pay in chat, and get pickup or delivery updates. Small businesses can start with QR codes or payment links before deeper integrations.

Delivering these journeys requires planning your integration end-to-end.

Integration and setup for businesses

A smooth setup depends on your market, payment methods, and the experience you want to build.

Integration models

You can integrate in different ways depending on your market and stack.

- UPI intent mode: In India, trigger UPI apps to complete payment and return confirmation to WhatsApp.

- Payment-gateway deep integration: Connect card, net banking, and UPI flows through your gateway for a fully in-chat experience.

- Developers can use WhatsApp Cloud API and payment partner SDKs to orchestrate status updates, order confirmations, and refunds.

If you need a faster path to market, payment links and QR flows can help you launch quickly.

Payment links and QR-code flows

For Brazil, Payment Links offer a fast path to launch. Generate a secure link through your gateway, share it in chat, and track the payment status while keeping customers updated on their order. With QR-code payments in India and Brazil, customers can scan a merchant QR in chat and pay without switching apps.

To make all of this easier, here’s how Infobip supports end-to-end onboarding.

Onboarding with Infobip

Infobip’s CX consultants handle implementation, development, payment partner linkage, testing, maintenance, and compliance. We design end-to-end journeys with Flows, chatbots, and agent handover so you can launch faster and scale with confidence.

With implementation planned, the next priority is keeping payments safe and compliant.

Security, compliance and limitations

Payments must be safe, compliant, and transparent. WhatsApp and payment partners provide strong controls, and you should layer in your own risk checks.

Security measures

All messages are end-to-end encrypted. Each transaction requires authentication, such as a UPI PIN or card authorization. You can enforce two-factor authentication, device checks, and session timeouts to reduce fraud.

Security is only part of the picture. Limits and fees also shape your payment experience.

Transaction limits and potential fees

Limits vary by country, bank, and partner. India commonly enforces ₹100,000 per transaction and daily caps for P2P. Brazil often has R$1,000 per transaction limits and monthly caps. P2P transfers are generally free. Merchants may pay processing fees set by gateways or acquirers.

It’s also important to understand today’s constraints and risks before you scale.

Limitations and risks

Availability is limited to specific countries. Regulations can change and may restrict features or volumes. International transfers and cross-border P2P are not supported today. Educate users about scams and only share payment details in verified chats.

Fraud prevention checklist

- Verify business profiles and display trust signals in chat

- Use official WhatsApp Business accounts with a display name and green check where eligible

- Require customer authentication for every transaction

- Notify customers instantly about payments and refunds

- Monitor anomalies and set velocity limits with your gateway

Looking ahead, WhatsApp’s roadmap will determine what you can do next with payments.

Future outlook and roadmap

Meta is expanding payments capabilities and exploring new models. Timelines vary by market.

Expansion targets

Markets like Mexico, the UK, the US, Guatemala, and Indonesia have been evaluated, but there are no official launch dates. Expect staggered rollouts once partners and regulators align.

Cross-border and stablecoin pilots

Meta is testing options for cross-border payouts and stablecoin-based micro-transactions. These could unlock new use cases like creator monetization, marketplace disbursements, and micro-tipping when regulations allow.

What businesses should do now

Design your payment flows, select vetted gateways, align on compliance, and build your conversational journey so you’re ready when new features land in your market.

These recommendations are already paying off for brands using WhatsApp payments.

Case studies

Tata AIA Life Insurance

Tata AIA integrated Payments on WhatsApp and turned messaging into a one-stop shop for policy renewals. With WhatsApp powered by Infobip, they boosted sales and revenue while giving customers convenience at their fingertips.

Payments on WhatsApp, with minimal steps and upfront confirmation, was much needed to boost confidence and satisfaction… Previously, customers had to log in, authenticate, and go through gateway processing. In three months, approximately 3,000 customers paid around Rs. 40 million for renewals. Infobip’s support made integration a breeze and drove increased sales and loyalty.

Mr. Sanjay Arora

Executive Vice President & Head of Operations at Tata AIA Life Insurance

Vai de Bus ticketing

Riders in Brazil can buy bus tickets in WhatsApp, receive confirmation instantly, and board with a digital pass. This reduces queues, lowers cash handling, and improves the rider experience.

SMBs using QR-code payments

Small merchants in India and Brazil share QR codes in chat, accept cards or supported bank payments, and send receipts instantly. This setup speeds checkout and cuts no-shows for bookings.