What is 2FA (Two-Factor Authentication), and how can you implement it?

Your customers’ security should be one of your highest priorities. Learn about 2FA and how it can help you protect your customers.

What does 2FA mean, and how does it work?

2FA is short for Two-Factor Authentication. It refers to a security process that requires users to provide two forms of identification to verify their identity before accessing an account or making a transaction. This extra layer of security typically involves using an online password and another device, like a mobile phone.

The most popular form of 2FA is when a customer logs in to their account using a password, after which they receive a one-time pin (OTP) to confirm their identity. An OTP or 2FA PIN is a code that is automatically generated and sent, usually to a mobile device, to allow a single login session or transaction.

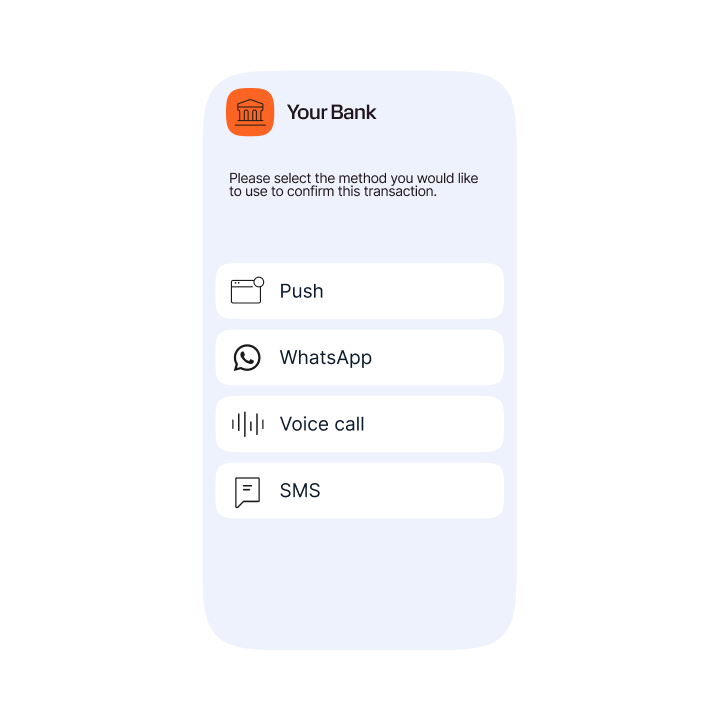

Here is an example of a 2FA process where customers can choose the channel they want to use for authentication:

Step 1: Users initiate the 2FA process and see a prompt asking them which channel they want to use.

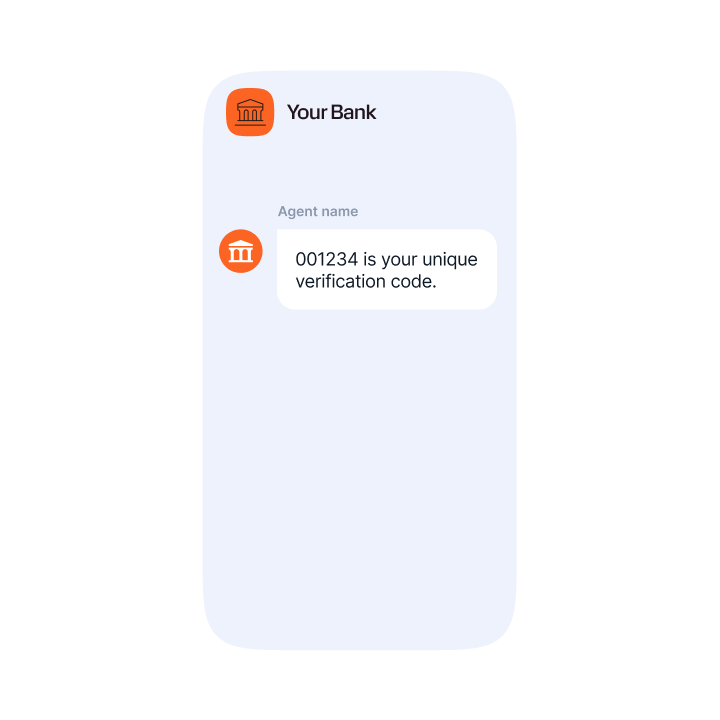

Step 2: After choosing the channel, users receive their verification code.

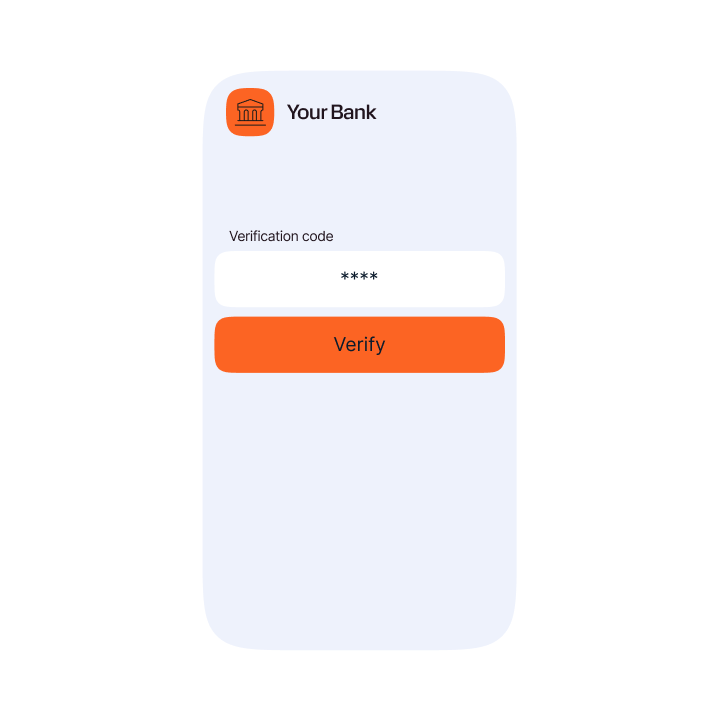

Step 3: Users enter the verification code in the app or web, authenticating the transaction.

The benefits of 2FA

The main benefit of 2FA is that it provides an extra layer of security, making it harder for attackers to access accounts. Simply adding a layer of 2FA to logins and transaction processes can alleviate risks of stolen data. According to Verizon, 80% of cyber breaches could be prevented by 2FA.

As a method of multi-factor authentication (MFA), it helps ensure online accounts and transactions are safe from fraudsters’ many tactics, including email phishing, smishing, and SIM swapping. Google reported that 100% of automated bots, 99% of phishing attacks, and 66% of targeted attacks were blocked by two-factor authentication.

Here is an overview of the benefits of 2FA in more detail:

1. Stronger security

It’s not easy for a hacker to bypass 2FA, making it an effective security tool against fraud. Hackers would have to know lots of information to gain access and duplicate information, not just one password.

Turning on two-factor authentication is an easy way to stay protected. Even the simplest form of 2FA puts a practically impenetrable wall between hackers and your customers’ personal information.

Taking these steps to protect your customers’ accounts will offer them the highest level of security and the best UX, creating happy and secure customers all around.

2. Improved user experience

The goal of 2FA is to secure personal information while still providing a smooth user experience. In the case of push notifications, there’s no need to enter a PIN to confirm the authentication. A simple click is all that’s required.

Tip: Using an omnichannel 2FA solution, you can allow customers to choose the channel that best suits them, putting UX and security first.

Example of an OTP code delivered on WhatsApp.

3. Increased productivity and flexibility

Companies that embrace new technology are likely to experience better productivity and flexibility. Customers can sign up for services faster and more securely than before.

Today, businesses use 2FA so their employees can securely access corporate applications, data, documents, and back-office systems from virtually any location without putting company data at risk.

4. Lower security management costs

Implementing 2FA can help reduce the lengthy and costly password reset calls and can act as a secure way for customers to sort these issues out themselves.

Reducing customer interactions with call centers, not only strengthens security but also improves UX. Then, as a massive bonus, operational overheads that are associated with security controls are reduced.

5. Improved customer trust

Having stronger security measures for ecommerce sites increases consumers’ trust. Consumers are more likely to trust other consumers on sites like eBay or PayPal knowing that everyone on the system must pass through the same tight security as they did. Building a large circle of trust within the community—especially with services like eBay and Etsy—is essential to these services’ long-term success.

Example use cases for 2FA

Banking & finance

It is common and crucial for banks and financial institutions to use 2FA services. From requiring a PIN to access your bank card, to a TOTP (time-based one-time password) to finalize money transfers, 2FA keeps customers’ banking information safe and secure.

Related customer story:

eCommerce

Online retailers often use 2FA during the login process. When credit card information can be saved and stored on their accounts, adding an extra layer of protection is essential for customers to feel safe buying from their sites.

Healthcare

Healthcare organizations are responsible for securing patient data and information. Using 2FA, they can reassure their patients that only they can access their medical records. 2FA is also required for doctors to access patient files.

Government

Governments have had to shift to using online and cloud-based platforms for people to access their government accounts. This can include anything from student loan accounts, retirement savings, applications for driver’s licenses, and other government services.

Governments have had to shift to using online and cloud-based platforms for people to access their government accounts. This can include anything from student loan accounts, retirement savings, applications for driver’s licenses, and other government services.

How to implement 2FA effectively

With almost 100% mobile phone ownership in most major markets, OTP (PIN codes) sent to a mobile device is the most common method of 2FA implementation.

However, it is crucial to choose the best channel for sending the PIN, depending on the individual use case and the preferences of each customer.

For example, some people may live or work in places with unreliable mobile or data signals. So, configuring a failover channel is key to ensuring that codes are delivered securely and before they expire in cases where time-based one-time PINs (TOTPs) are used.

The most popular methods of 2FA include:

- SMS 2FA

- Email 2FA

- RCS 2FA (OTP)

- Voice 2FA (OTP)

- Mobile Push notifications

- Sending OTPs via chat apps like WhatsApp, Viber, Zalo, KakaoTalk and others

You should ensure 2FA is used as effectively and efficiently as possible to ensure your customers do not get inconvenienced and associate increased security with increased hassle.

An effective authentication solution should be able to automatically select the best primary and failover channel and trigger delivery of the OTP on the second channel when the first is not successful. This ensures that 2FA PIN codes are always delivered.

This is where a flexible omnichannel authentication solution becomes crucial, as it reduces the overall overhead for the organization by ensuring that human intervention is only required when necessary.

How Infobip can help you with 2FA

At Infobip, we help businesses from global brands to independent retailers secure their customers and transactions. Our solution, Infobip Authenticate, is unique in the market as it incorporates multiple channels and analyses various factors, including cost and popularity, to determine the best channel for each OTP.

Infobip’s 2FA messaging solutions for OTP delivery include SMS OTP, RCS OTP, WhatsApp OTP, Voice OTP, Viber OTP, Zalo OTP and KakaoTalk. This breadth of channels ensures that your OTPs are always delivered promptly and reliably in every destination.

Crucially, the solution is designed to blend seamlessly into existing business processes so that your customers benefit from an easy and consistent experience that reduces friction all the way from account registration to purchase.

Just some of the brands that trust Infobip to help with their authentication challenges include:

- Uber: Protecting customers with call anonymization and number masking.

- Leanpay: Helping to support a 20% month-on-month growth in registered users with two-factor authentication.

- Bukalapak: Improved user security AND increased delivery rates.

- Nickel: Simplified onboarding and cost optimizations with SMS 2FA solution.

- Yousign: Increasing one-time PIN (OTP) delivery rates to over 97% via SMS and text-to-speech (TTS) failover.

To conclude: by implementing quality 2FA solutions, you are signaling to customers and users that you take security seriously. This is increasingly important as we trust more of our digital lives to online services.

Explore our omnichannel 2FA solution

Verify your customers effortlessly using Infobip Authenticate, a robust omnichannel 2FA solution that provides a fully automated, cost-effective way to authenticate customers.

Other questions regarding 2FA:

This article was last updated in October 2024 to include more tips on 2FA implementation.

Learn how to launch your first SMS campaign with Infobip in just a few easy steps: